NEWS & TECHNOLOGY PROCESSES

TSMC takes market from Samsung, GloFo, but Covid-19 impact to come

By Peter Clarke Foundry revenues are up 30 percent year-on-year in the

first quarter of 2020 but the Covid-19 pandemic could

hinder future market demand, according to TrendForce.

The biggest success in the top ten foundries was market

leader TSMC which continued to take market share from its

closest competitors Samsung and Globalfoundries.

Other successful companies

included Powerchip Semiconductor

Manufacturing Corp. (PSMC) and United

Microelectronics Corp. both also of Hsinchu

in Taiwan.

TrendForce reckons the foundry industry

overall benefited from clients stockpiling

chips. Poor performers year-on-year

included Tower Semiconductor Ltd. and

Hua Hong.

Now the whole of the foundry market

will face a challenge, as the Covid-19

pandemic has caused a reduction in the

demand for end products. The impact on

foundries is expected to come in 2Q20,

the market research firm said.

TrendForce said that strong demand for TSMC’s 7nm manufacturing

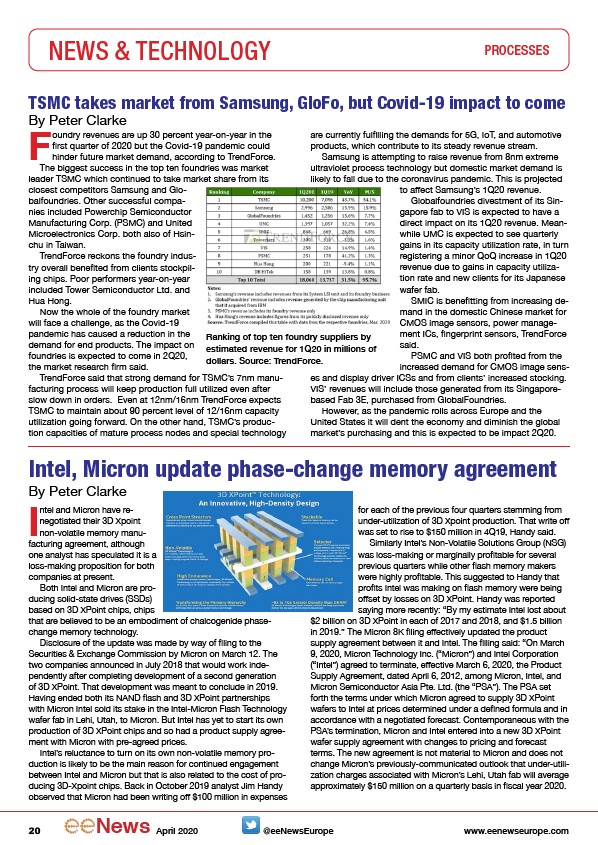

Ranking of top ten foundry suppliers by

estimated revenue for 1Q20 in millions of

dollars. Source: TrendForce.

process will keep production full utilized even after

slow down in orders. Even at 12nm/16nm TrendForce expects

TSMC to maintain about 90 percent level of 12/16nm capacity

utilization going forward. On the other hand, TSMC’s production

capacities of mature process nodes and special technology

are currently fulfilling the demands for 5G, IoT, and automotive

products, which contribute to its steady revenue stream.

Samsung is attempting to raise revenue from 8nm extreme

ultraviolet process technology but domestic market demand is

likely to fall due to the coronavirus pandemic. This is projected

to affect Samsung’s 1Q20 revenue.

Globalfoundries divestment of its Singapore

fab to VIS is expected to have a

direct impact on its 1Q20 revenue. Meanwhile

UMC is expected to see quarterly

gains in its capacity utilization rate, in turn

registering a minor QoQ increase in 1Q20

revenue due to gains in capacity utilization

rate and new clients for its Japanese

wafer fab.

SMIC is benefitting from increasing demand

in the domestic Chinese market for

CMOS image sensors, power management

ICs, fingerprint sensors, TrendForce

said.

PSMC and VIS both profited from the

increased demand for CMOS image senses

and display driver ICSs and from clients’ increased stocking.

VIS’ revenues will include those generated from its Singaporebased

Fab 3E, purchased from GlobalFoundries.

However, as the pandemic rolls across Europe and the

United States it will dent the economy and diminish the global

market’s purchasing and this is expected to be impact 2Q20.

Intel, Micron update phase-change memory agreement

IBy Peter Clarke ntel and Micron have renegotiated

their 3D Xpoint

non-volatile memory manufacturing

agreement, although

one analyst has speculated it is a

loss-making proposition for both

companies at present.

Both Intel and Micron are producing

solid-state drives (SSDs)

based on 3D XPoint chips, chips

that are believed to be an embodiment of chalcogenide phasechange

memory technology.

Disclosure of the update was made by way of filing to the

Securities & Exchange Commission by Micron on March 12. The

two companies announced in July 2018 that would work independently

after completing development of a second generation

of 3D XPoint. That development was meant to conclude in 2019.

Having ended both its NAND flash and 3D XPoint partnerships

with Micron Intel sold its stake in the Intel-Micron Flash Technology

wafer fab in Lehi, Utah, to Micron. But Intel has yet to start its own

production of 3D XPoint chips and so had a product supply agreement

with Micron with pre-agreed prices.

Intel’s reluctance to turn on its own non-volatile memory production

is likely to be the main reason for continued engagement

between Intel and Micron but that is also related to the cost of producing

3D-Xpoint chips. Back in October 2019 analyst Jim Handy

observed that Micron had been writing off $100 million in expenses

for each of the previous four quarters stemming from

under-utilization of 3D Xpoint production. That write off

was set to rise to $150 million in 4Q19, Handy said.

Similarly Intel’s Non-Volatile Solutions Group (NSG)

was loss-making or marginally profitable for several

previous quarters while other flash memory makers

were highly profitable. This suggested to Handy that

profits Intel was making on flash memory were being

offset by losses on 3D XPoint. Handy was reported

saying more recently: “By my estimate Intel lost about

$2 billion on 3D XPoint in each of 2017 and 2018, and $1.5 billion

in 2019.” The Micron 8K filing effectively updated the product

supply agreement between it and Intel. The filling said: “On March

9, 2020, Micron Technology Inc. (“Micron”) and Intel Corporation

(“Intel”) agreed to terminate, effective March 6, 2020, the Product

Supply Agreement, dated April 6, 2012, among Micron, Intel, and

Micron Semiconductor Asia Pte. Ltd. (the “PSA”). The PSA set

forth the terms under which Micron agreed to supply 3D XPoint

wafers to Intel at prices determined under a defined formula and in

accordance with a negotiated forecast. Contemporaneous with the

PSA’s termination, Micron and Intel entered into a new 3D XPoint

wafer supply agreement with changes to pricing and forecast

terms. The new agreement is not material to Micron and does not

change Micron’s previously-communicated outlook that under-utilization

charges associated with Micron’s Lehi, Utah fab will average

approximately $150 million on a quarterly basis in fiscal year 2020.

20 News April 2020 @eeNewsEurope www.eenewseurope.com

/eenewseurope

/www.eenewseurope.com